Trading performance metrics are the numbers that show whether a strategy is actually profitable, repeatable, and risk-aware over time. Unlike win rate alone, metrics like expectancy, profit factor, drawdown, and risk-adjusted return reveal whether a system has a real edge.

Why the win rate alone can mislead traders

A high win rate does not automatically mean a strong trading system. It is the industry's most successful illusion. Retail traders often obsess over "hitting" 80% or 90% of their trades, treating the win rate as a psychological scoreboard.

The Mathematical Illusion of High Win Rates

A strategy can win 90% of the time and still be mathematically bankrupt. If your average loss is ten times larger than your wins, a single bad trade can annihilate weeks of progress. Professional evaluation ignores the "frequency" of success to find the true robustness of the system.

To strip away the emotional attachment to "being right," consider two contrasting models:

- Strategy A (The Illusion): 80% win rate. It wins $100 eight times but loses $500 twice. Total result: -$200. Despite "winning" most of the time, the account is bleeding.

- Strategy B (The Edge): 40% win rate. It wins $400 four times and loses $100 six times. Total result: +$1,000. While it feels like "losing" more often, the business is thriving.

The obsession with hitting a high percentage transforms trading into a psychological trap. Professionals manage the Expectancy - the average dollar value you expect to make per trade, rather than the frequency of the wins.

Professional trading is not a game of being right most often, but a disciplined calculation of how much you capture when the market moves in your favor versus how little you surrender when it doesn't.

What Makes a Trading Metric Actually Useful?

Before we crunch the numbers, we need to separate professional-grade intelligence from "vanity" stats. A metric is only valuable if it acts as a cold, mathematical mirror of your strategy’s health. To move from "guessing" to "governing" a portfolio, every data point must clear one of these five filters:

- Edge (Expectancy): Does this system actually have a positive return over time? If a metric doesn't prove you’re playing a game you can win, it’s noise.

- Risk (Exposure): What is the "hidden cost" of your profit? We need to know exactly how much capital is at risk so one bad outlier doesn’t end the business.

- Consistency (Reliability): Is this a repeatable process or just a few lucky trades? We prioritize metrics that reward steady, linear growth and penalize erratic behavior.

- Efficiency (Opportunity Cost): How hard is your money working? A 10% return with tiny drawdowns is objectively better than a 20% return that requires surviving a 30% crash.

- Survivability (The Point of Ruin): How close are you to total depletion? This filter measures your distance from a "worst-case" market regime.

By using these filters, we stop treating trading like a psychological scoreboard and start treating it like a sovereign fund.

The 7 Trading Metrics That Actually Matter More Than Win Rate

Moving beyond the "" illusion requires a shift toward institutional-grade analysis. To evaluate a strategy's true robustness, you must look at how it handles risk, recovers from stress, and generates mathematical expectancy.

1. Expectancy (The Profitability Per Trade)

Expectancy defines the average dollar amount you can expect to make or lose on every trade you take.

- The Logic: (Win Rate × Average Win) - (Loss Rate × Average Loss).

- Why it matters: It is the ultimate diagnostic of "Edge." If your expectancy is negative, you aren't trading, but just slowly burning capital.

- What is "Healthy": Any positive number is an edge, but serious operators look for a high enough expectancy to cover commissions, slippage, and execution errors.

- Interpretation: Expectancy must be viewed alongside trade frequency. A high expectancy is useless if the strategy only triggers once a year.

2. Profit Factor (The Efficiency Ratio)

This metric represents the ratio of gross profit to gross loss over a specific period.

- The Logic: Gross Profit / Gross Loss.

- Why it matters: It measures the "return on stress." It tells you how many dollars you earn for every dollar you surrender to the market.

- What is "Healthy": A value of 1.41 to 2.0 is considered strong. Values above 3.0 often suggest a small sample size or an "overfitted" strategy that won’t survive live markets.

- Interpretation: Always check Profit Factor against Total Trades. A high factor over only 10 trades is statistically insignificant.

3. Maximum Drawdown (The Survivability Floor)

Maximum Drawdown (MDD) is the largest peak-to-trough decline in your account equity before a new peak is achieved.

- The Logic: (Peak Value - Trough Value) / Peak Value.

- Why it matters: It defines the "pain threshold." Professional allocators prioritize MDD because it reveals the true risk of ruin and the psychological toll of the strategy.

- What is "Healthy": Institutional mandates often cap MDD at 10–15%. For retail operators, a drawdown exceeding 25% usually triggers a fundamental review of the system.

- Interpretation: MDD should be compared to the Recovery Factor to see how long the strategy stays "underwater."

4. Average Win / Average Loss Ratio (The R-Multiple)

This ratio reveals the structural payoff of your strategy by comparing the size of your winners to your losers.

- The Logic: Average Gain per Winning Trade / Average Loss per Losing Trade.

- Why it matters: It tells you if you are a "Sniper" (large wins, low frequency) or a "Grinder" (small frequent wins).

- What is "Healthy": A ratio of 2:1 or higher is the gold standard for trend followers. Scalpers might survive on 1:1 if their win rate is exceptionally high.

- Interpretation: This is the "balancing scale" for win rate. If your win rate drops, your Win/Loss ratio must increase to maintain a positive expectancy.

5. Sharpe Ratio (Risk-Adjusted Performance)

The Sharpe ratio measures the excess return of a strategy relative to its volatility (Standard Deviation).

- The Logic: (Strategy Return – Risk-Free Rate) / Standard Deviation of Returns.

- Why it matters: It filters out "lucky" traders who make money simply by taking massive, erratic risks. It rewards consistency over "lumpy" gains.

- What is "Healthy": A Sharpe ratio above 1.0 is acceptable; above 2.0 is excellent.

- Interpretation: Sharpe can be deceptive for strategies with "fat tails" (occasional huge wins), as it penalizes upward volatility as much as downward risk.

6. Sortino Ratio (The Downside Specialist)

A variation of the Sharpe ratio that only penalizes the strategy for "harmful" volatility.

- The Logic: (Strategy Return - Target Return) / Downside Deviation.

- Why it matters: Serious traders don't mind "volatility" if it’s to the upside. The Sortino ratio provides a more realistic picture of risk for capital preservation.

- What is "Healthy": A Sortino ratio above 2.0 is typically the target for professional strategy operators.

- Interpretation: If your Sortino is significantly higher than your Sharpe, it means your strategy has a lot of "good" upside volatility (large runners).

7. Recovery Factor (The Resilience Metric)

This shows how many times the net profit exceeds the maximum drawdown experienced.

- The Logic: Total Net Profit / Maximum Drawdown.

- Why it matters: It tells you if the "gain was worth the pain." It measures how efficiently the strategy "earned back" its worst loss.

- What is "Healthy": A Recovery Factor above 3.0 over a significant period is a sign of a very robust and resilient system.

- Interpretation: Use this to rank strategies. If two systems have the same profit, the one with the higher Recovery Factor is the superior choice for capital allocation.

While the crowd is blinded by the flash of high-level winnings, the disciplined trader listens to the heartbeat of these indicators, knowing that true mastery lies in the unwavering grace of a strategy that weathers the inevitable market storms.

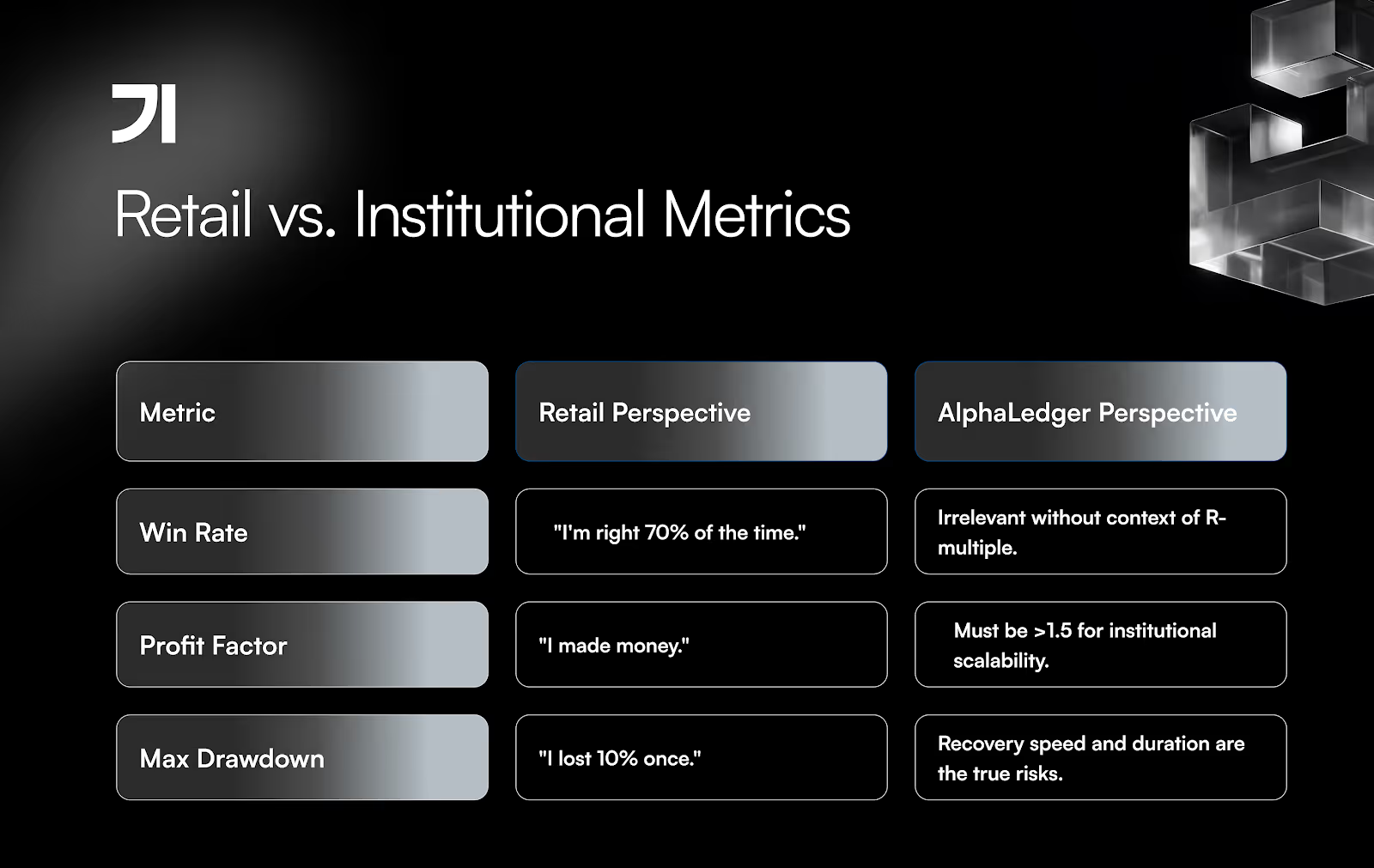

Institutional vs. Retail Perspectives

To understand where your strategy truly stands, it is essential to bridge the gap between simple surface-level tracking and the rigorous performance intelligence that professional allocators require.

Why these metrics matter more when looked at together

In trading, numbers never live in a vacuum. A system's true strength reveals itself only in the symphony of its indicators.

The Fragility of "Perfect" Performance

A high Sharpe Ratio paired with a Profit Factor near 1.1 is a trap. Such a system is exceptionally fragile. The slightest shift in market volatility will transform "stability" into a series of uncontrollable losses.

The Psychological Toll of Expectancy

Mathematically flawless Expectancy does not guarantee success if it is accompanied by a Deep Drawdown. Most traders surrender psychologically long before the positive math has a chance to play out.

When Win Rate Masks Failure

A high Win Rate with a weak Average Win/Loss ratio is a ticking time bomb. It creates an illusion of mastery until a single "black swan" exposes the structural weakness of your architecture.

Trading is not the search for a perfect number, but the art of balance. The best strategy is not the one with the highest peak, but the one that allows you to stay in the game during the worst of storms.

What serious traders should track before seeking outside capital

To attract institutional allocators, you must move beyond the "P&L screenshot." Professionals don’t buy stories of massive gains. Еhey buy robustness, transparency, and repeatability. Being "investor-ready" requires performance intelligence that a basic spreadsheet cannot capture.

Consistency Across Time

Investors prioritize strategies that survive various market regimes - volatility spikes and trend reversals. Maintaining a positive expectancy over months is infinitely more valuable than a lucky, isolated 200% return.

Drawdown Control and Recovery

Risk is a measure of your behavior under pressure. Allocators focus on Maximum Drawdown and the Recovery Factor to ensure a market anomaly won't lead to a total capital wipeout.

Risk-Adjusted Performance

Sophisticated players use Sharpe and Sortino ratios to distinguish genuine skill from excessive, unmanaged risk. They need to know if your returns are repeatable or merely a result of luck.

Verified Performance History

The gold standard is an Audited Track Record. Investors need certainty that results are not "cherry-picked," requiring a verified history generated through a transparent, professional process.

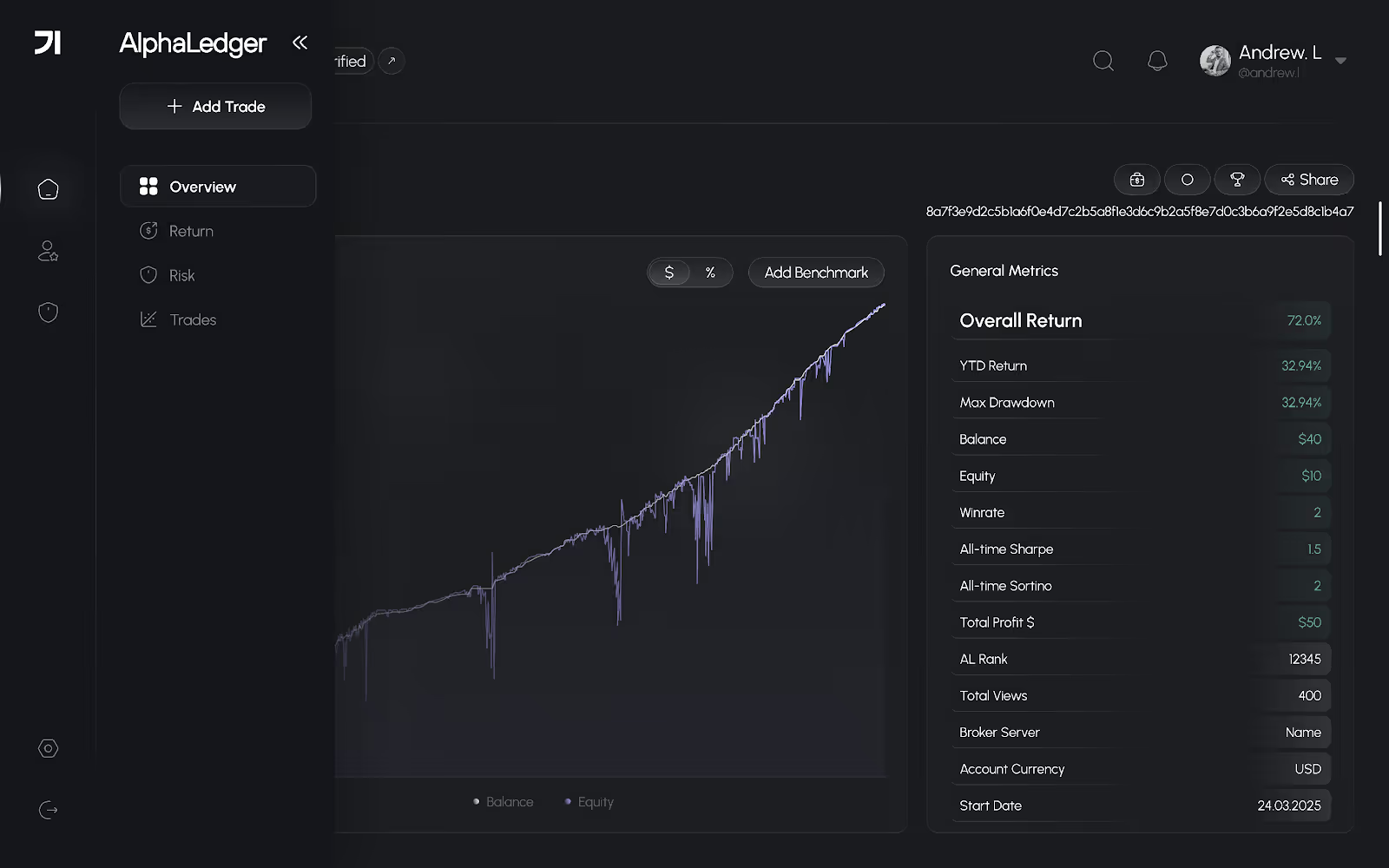

AlphaLedger: Your Pathway to Institutional Discovery

Moving from retail guesswork to institutional-grade execution requires a specialized environment designed for deep performance intelligence.

AlphaLedger serves as this cognitive layer, closing the gap between strategy operators and global capital by transforming raw trade data into high-authority analytical reporting.

Instead of focusing on whether you were "right" today, the platform enables you to:

- Track Real-Time Performance (Automated Analytics): Instantly connect your MT4/MT5 accounts to monitor live equity curves and expectancy shifts without manual spreadsheets.

- Analyze Beyond Surface-Level P&L: Automatically calculate all 7 critical metrics, including Profit Factor and Sortino Ratio, to instantly verify if your returns are a result of genuine edge.

- Understand Behavioral Patterns: Identify execution errors and behavioral "leaks" that standard brokerage statements often mask.

- Build a Credible Performance Record (Investor-Ready): Transition from a "trader" to a verified strategy operator with CPA-ready audit workflows and transparency standards required for Institutional Capital Allocation.

By shifting the focus from the vanity of a win rate to the reality of risk-adjusted returns, AlphaLedger transforms your trading into a data-driven business.

Connect your account to see the metrics that actually define trading performance.

Strategic FAQ

Q: Why is win rate a misleading trading metric?

A: Because it only shows how often you win, not the magnitude of those wins versus losses. A 90% win rate can still blow up an account if the 10% of losses are catastrophic.

Q: What metric matters more than win rate?

A: Expectancy and profit factor. They provide a complete picture of mathematical edge and strategy scalability.

Q: What is a good profit factor?

A: Anything above 1.0 is profitable, but professional systems generally target 1.5 or higher for sustainable growth.

Q: Why do risk-adjusted returns matter?

A: They show how much you earned relative to the emotional and financial stress (volatility/drawdown) required to get there.

Q: How can I present my performance more credibly?

A: By providing verified, deep-level analytics and audited reporting instead of isolated screenshots.

Mastering these 7 metrics doesn't make you a better guesser - it makes you a verifiable business. Disciplined traders build audited systems that attract institutional capital. This is the cognitive edge that turns performance into portfolio